By Michelle Andrews, Kaiser Health News

Health insurance premiums and deductibles for job-based coverage edged upward in 2019, surpassing increases in both wages and inflation, according to an annual employer survey of more than 2,000 employers released Wednesday. But the results were uneven, and many workers least able to afford it were confronted with higher-than-average costs.

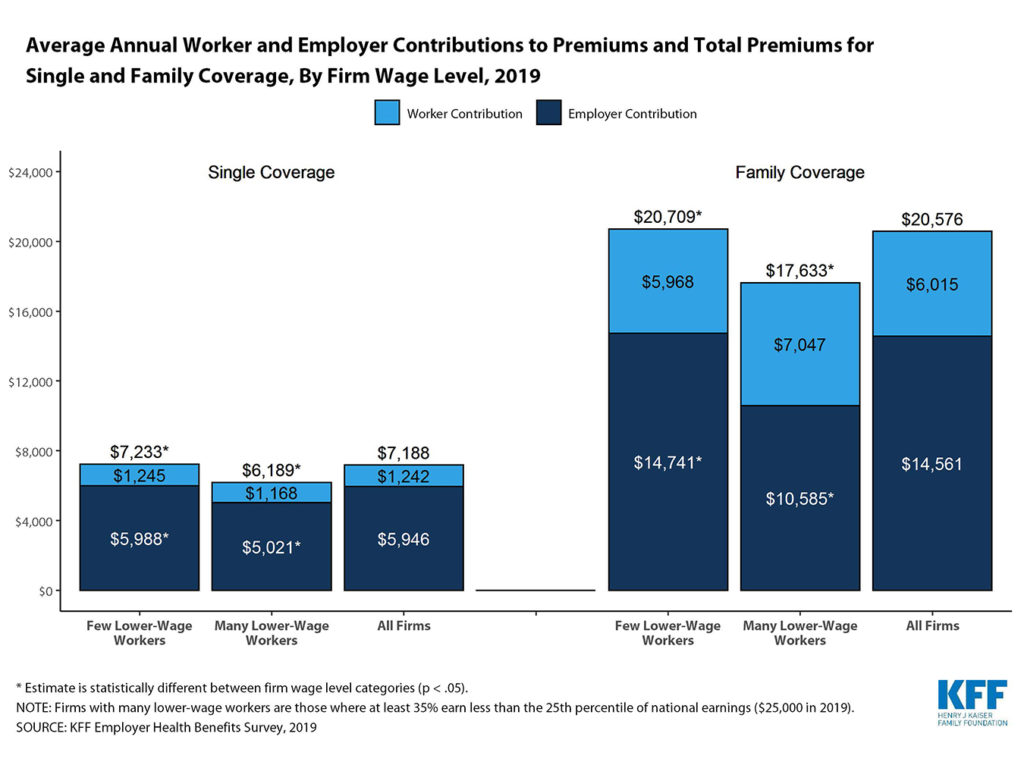

People at companies with large numbers of lower-wage employees faced bigger deductibles for single coverage and were asked to pony up a larger share of their incomes to pay premiums than those at firms with fewer people with low earnings, according to the annual employer health benefits survey by the Kaiser Family Foundation. (KHN is an editorially independent program of the foundation.)

The survey defined companies with many lower-wage workers as those with at least 35% of employees earning $25,000 or less annually. This includes many restaurants and retail businesses, personal care service companies, and building and grounds cleaning and maintenance businesses, among others.

More than 150 million people get health coverage through plans offered by their jobs.

The survey found that the average family coverage ran $20,576 in 2019, a 5% increase over last year. Workers paid nearly 30% of the total, or $6,015, on average.

The average premium for single coverage rose 4%, to $7,188, and workers paid $1,242 of that amount, or about 18% of the total. During the same period, inflation and wages grew at a slower rate, rising 2% and 3.4%, respectively, a pattern that has remained consistent over the past several years.

The average deductible for single coverage was $1,655, an amount that has increased by more than a third in the past five years. More than 40% of covered workers had deductibles of at least $2,000 in 2019.

Many workers face charges in addition to a deductible. Eighty-five percent of covered workers owed more if they were hospitalized. The amounts varied depending on the plan, from an average 20% coinsurance charge to an average $326 copayment. Two-thirds of covered workers also faced a $25 copayment for doctor’s office visits, while a quarter faced a coinsurance charge of 18%, on average.

As presidential candidates discuss adopting a “Medicare for All” approach that would move people into government-sponsored coverage, one of the arguments against it is that people would lose their employer-sponsored insurance. But employer coverage varies.

“There are a lot of people who feel pretty well serviced by their coverage,” said Gary Claxton, a senior vice president and director of the Program on the Health Care Marketplace at the Kaiser Family Foundation, who co-authored the study and an accompanying article in the journal Health Affairs. “But there are a lot of people for whom it’s a little more challenging in terms of affordability and the protection their coverage provides.”

Fewer workers at companies with large numbers of lower-wage workers were eligible for coverage in the first place, the survey found. Overall, 57% of companies offer health insurance to their workers. But only two-thirds of workers at lower-wage firms that offered coverage were eligible for it, compared with 81% of workers at other firms, according to the survey. Companies may restrict coverage for workers who are part-time, temporary or newly employed, for example.

Workers allowed to sign up for a lower-wage firm’s plan may find it takes a relatively bigger bite out of their paychecks than workers at other companies.

While the total premium for coverage at these companies is less on average than premiums at companies who have few low-wage earners, workers must pay a bigger share of the cost. For family coverage, workers are on the hook for 41% of the full cost, or $7,047, compared with a 30% share for workers at other firms, or $5,968. (Workers’ share of the premium for single coverage is much less varied: 18%, or $1,245, at companies with few low-wage workers versus 19%, or $1,168, at companies with many low-wage workers.)

“Costs are prohibitive when workers making $25,000 a year have to shell out $7,000 a year just for their share of family premiums,” Drew Altman, KFF president and CEO, said in a press release announcing the study’s release.

One way to help reduce the costs for lower-income workers is to base the amount of their premium contributions on their wages, said Brian Marcotte, president and CEO of the National Business Group on Health, which represents the interests of very large employers, mostly with at least 10,000 employees.

In 2019, about a third of those employers used a wage-based sharing formula to calculate employee costs. Though typically applied to premium contributions, such a model may also be used to determine deductibles, out-of-pocket maximums or the amount an employer contributes to health savings accounts.

Deductibles are more prevalent and may be more costly at lower-wage firms than at companies with higher wages. The deductible for single coverage, for example, is at least $1,000 more on average at lower-wage firms: $2,679 vs. $1,610.

Given the likelihood of the expense of premium contributions and deductibles, perhaps it’s no surprise that many workers at lower-wage companies choose not to sign up for coverage even if it’s offered.

Only a third of workers at such companies that offered health insurance signed up, the survey found. At higher-wage companies, the figure was significantly more: 63%.

This year, for the first time since the Affordable Care Act was passed, workers no longer faced a tax penalty for not having health insurance. Nine percent of employers with at least 50 workers that offered health insurance reported they thought the elimination of the penalty reduced the percentage of workers who signed up for coverage.

In addition to being unaffordable for many people, coverage at these lower-wage firms may not be especially comprehensive, Claxton said.

“Premiums are lower in low-wage companies because the coverage probably isn’t very good,” he said.

“Basically, the company is saying [to workers], ‘Don’t buy it,’” said Claxton. “And they don’t.”

Kaiser Health News (KHN) is a national health policy news service. It is an editorially independent program of the Henry J. Kaiser Family Foundation which is not affiliated with Kaiser Permanente.