By Michael Ollove, Stateline

A patient waits to be admitted to the emergency room at the Los Alamitos Medical Center in Los Alamitos, California. Researchers worry that some state laws to protect patients from surprise medical bills, which often follow emergency medical situations, could inflate overall health care costs.Kirby Lee The Associated Press

New state laws designed to protect patients from being hit with steep out-of-network medical bills may contribute to higher health care costs and premiums, some researchers warn.

Lawmakers and advocates who pushed for surprise billing laws say the measures have protected consumers from some of the most egregious bills, which can climb into the hundreds of thousands of dollars. But some researchers recently have raised alarms that doctors and other medical providers are leveraging state laws that rely on arbitration to increase in-network fees, thereby raising health care costs for everyone.

Stacey Pogue, a senior policy analyst at Every Texan, a social justice organization that pushed for a surprise billing law in Texas, said such measures “did the most necessary thing of protecting consumers.” But Pogue also acknowledged there may be unintended consequences. “We were also concerned about inflationary costs, and the jury is out on that,” she said.

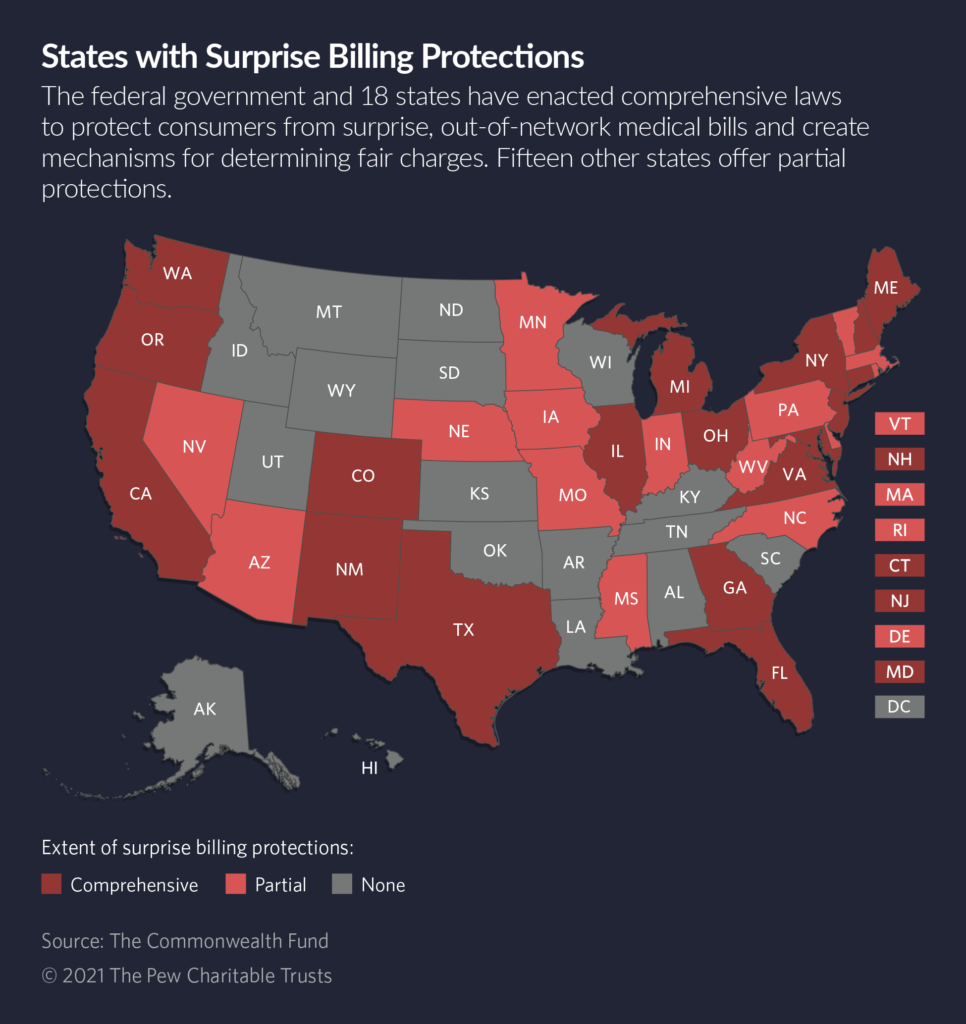

Eighteen states have passed surprise billing laws since 2014, most of them in the past three years. Last year, former President Donald Trump signed a federal version that covers self-funded health plans, including those offered by many employers, as opposed to the individual and commercial health plans regulated by states.

The concerns stem from guidelines states have established to help impartial arbitrators resolve disputes between providers and insurance carriers over how much should be paid for surprise, out-of-network bills.

“An upward trend in payments for out-of-network care could push rates higher in in-network contracts,” health policy researchers at Georgetown University wrote in a blog post last month. “These costs, in turn, could push premium costs higher for employers and consumers.”

Out-of-Network

Surprise billing occurs when patients are unaware that the medical provider treating them is not associated with their insurer, potentially exposing them to fees higher than in-network rates.

A typical example is when patients in an emergency room are seen by a physician who is not in their insurance company’s network. Another is when patients are having a surgery in an in-network hospital, but one member of a surgical team—say, the anesthesiologist—is out-of-network.

In many of those cases, even if the patient is somehow aware a doctor is out-of-network—which often is not the case—it isn’t reasonable to expect the patient to shop around for an in-network doctor. Patients rushed into an emergency room in cardiac arrest can’t be expected to survey emergency room doctors to determine who is in their insurer’s network. Sometimes, they aren’t even conscious.

A joint 2020 study from the Peterson Center on Health Care and the Kaiser Family Foundation found that 1 in 5 emergency medical claims and 1 in 6 hospitalizations in the U.S. included at least one out-of-network bill.

The problem worsened in the past decade, analysts say. The evolution is an outgrowth of insurance carriers using smaller networks of providers and the conviction among many doctors, particularly emergency room physicians and anesthesiologists, that insurers pay in-network providers unreasonably low rates.

In Congress and state legislatures, the debate has been waged not between political parties but rather between insurance carriers and groups representing doctors, each of which blames the other for causing the surprise billing problem.

“As we see it, the issue of surprise bills is related to abusive insurer tactics,” said Dr. Beverly Philip, president of the American Society of Anesthesiologists. “Insurers have offered contracts that are so below market rates that physicians cannot participate” in insurance networks, Philip said.

But Jeanette Thornton, a senior vice president at the America’s Health Insurance Plans, which lobbies for insurers, said doctors are to blame.

“Certain specialists like ER doctors and anesthesiologists use surprise billing to drive up their in-network rates,” she said.

State legislators in several states said reaching compromise on the bills was a long and unusually contentious process. “I was told it was never going to get done,” said Texas Republican state Sen. Kelly Hancock, who began sponsoring legislation as a House member in 2009 and finally got a comprehensive bill passed in 2019.

Baseball-Style Arbitration

Many of the states with comprehensive surprise billing laws protect patients from receiving bills that are higher than what they would pay for treatments from an in-network provider. That still leaves it up to insurers and out-of-network providers to hash out how much that provider should be paid. The state laws determine how to resolve those disputes.

Many states, including New Jersey, New York and Texas, use so-called baseball-style arbitration. Under that scenario, each side makes a proposal and the arbitrator picks one. The arbitrator is not permitted to split the difference or impose some other settlement amount.

States that use the arbitration method spell out in law the guidelines that arbitrators should use. States that don’t use arbitration set a benchmark for how much an insurer must pay a provider for out-of-network services in surprise billing scenarios.

STATELINE STORY April 22, 2020Many Health Providers on Brink of Insolvency

STATELINE STORY March 8, 2021Biden Aims to Build on Obamacare’s Cost-Cutting Measures

In states with and without arbitration, the biggest fights revolved around what benchmarks would be used to determine a fair rate for out-of-network services.

Not surprisingly, insurers pushed for the cheapest benchmark, which generally were the rates paid by Medicare. For hospital services, that is about half as much as the rates paid by private insurance, according to the Kaiser Family Foundation. That was anathema to providers.

Doctor groups favored an average of the amount other providers charged for a comparable service, a proposal that drew derision from insurers and many state legislators and officials. They argued that the amount doctors bill often bears little relationship to what insurers pay.

“Providers like to pretend charges reflect something, but they are just charges,” said Paige Duhamel, health care policy manager in New Mexico’s Office of Superintendent of Insurance. The state agency spearheaded the effort on surprise billing legislation, which passed in 2019 after a three-year effort. “I could never get a good explanation of that,” Duhamel said of providers’ focus on charges.

States that enacted surprise billing laws rejected insurers’ and doctors’ arguments, and instead adopted different standards.

The laws in New Jersey, New York and Texas all direct arbitrators to consider choosing the side that comes closest to the 80th percentile of the charges billed for a service in a geographic area. New Mexico, which doesn’t use arbitration, sets the rate at the 60th percentile of the amount commercial insurers pay.

California, also a non-arbitration state, sets payment for nonemergency, out-of-network services at 125% of the Medicare rate or the health plan’s average in-network rate, whichever is greater.

Researchers say the danger of inflation occurs mainly in the states that use arbitration and any payment standard that is higher than the in-network rate.

“If you create a system where the standard is greater than the in-network rate, then that becomes the benchmark,” said Loren Adler, associate director of the University of Southern California-Brookings Schaeffer Initiative for Health Policy, who studies surprise medical billing.

If out-of-network doctors consistently receive higher payments than in-network doctors, Adler said, in-network doctors will use those results as leverage to try to get higher rates in their negotiations with insurers—or they will refuse to be in networks altogether. That results in higher premiums or costs for patients.

STATELINE STORY April 5, 2019Surprise Medical Billing: Some States Ahead of Feds

Georgetown’s Jack Hoadley, who studies health insurance and co-wrote the blog on surprise billing, agreed that payment guidelines above network rates will have the effect of driving up health care costs. “If I’m confident I can get 80% of billed charges going through arbitration, I’m not going to settle for 50% in-network negotiations,” he said.

In his research, Adler has found that arbitration decisions are coming in above in-network rates.

Analyzing New York’s data from 2016 to 2018 after it enacted its surprise billing law, Adler and his fellow researchers found that arbitration decisions have averaged 8% higher than the 80th percentile of charges.

In another paper about New Jersey, which implemented its surprise billing law in 2018, Adler and his co-authors found that the median arbitration decisions were 5.7 times the prevailing in-network rates for the same services.

Federal Standards

The federal surprise billing law does not include the payment guidelines that researchers, including those at Georgetown, caution could lead to inflation.

Under the federal law, arbitrators can use the health plan’s in-network rate as a guide and use it to consider the provider’s experience and the complexity of the case. However, the federal law does not permit arbitrators to consider billed charges or Medicare and Medicaid rates.

Both Hoadley and Adler think the federal law is crafted in a way that will relieve inflationary pressure. “I’m hopeful the federal law works out better for patients than either New York or New Jersey,” Adler said.

Some state lawmakers, regulators and consumer advocates say the inflationary fears over the state surprise billing laws are unfairly overshadowing a big win for consumers.

The Texas Department of Insurance, for example, reports that between January 2020, when the law was implemented, and the following October, the average arbitrator decision was for $967, compared with the original average surprise bill amount of $2,775.

Hancock and other supporters say the law has had an even more beneficial impact: driving settlements prior to arbitration. According to the Texas insurance department, the average bill in cases settled before arbitration was $2,537 and the average settlement amount was $763.

Elisabeth Benjamin, vice president of health initiatives at the Community Service Society of New York, an anti-poverty organization that pushed for the state law in New York, said such results prove that surprise billing laws are protecting patients from outrageous surprise bills. And even if they contribute to some inflation in health spending, it is negligible compared with other factors contributing to America’s high health care costs.

“I just feel like it’s a cheap shot to say surprise billing laws are inextricable to the rise of health care costs,” she said. “That’s the problem? I don’t think so.”